- Global Markets Investor

- Posts

- The S&P 500 rose for the 4th straight week. Weekly market recap, trading week 17/2026

The S&P 500 rose for the 4th straight week. Weekly market recap, trading week 17/2026

Summary of the trading week using the most popular posts from the X platform

Global Markets Investor

April 26, 2026

In partnership with

GLOBAL MARKETS INVESTOR’S PORTFOLIO IS 🔥UP +93%🔥 SINCE JANUARY 2024

DURING THE MARCH-APRIL 2025 MARKET TURMOIL, MAJOR US INDEXES FELL NEARLY 20%, WHILE THE GMI PORTFOLIO GAINED OVER 5%, FIND OUT HOW BELOW:

In this series, you can find financial markets posts with the highest number of interactions from my X platform feed over the most recent week. I am aware that not everybody uses X regularly, so I thought it could provide some value to your analysis and investment process. These posts are surrounded by extra charts, commentary, and explanations of complicated topics.

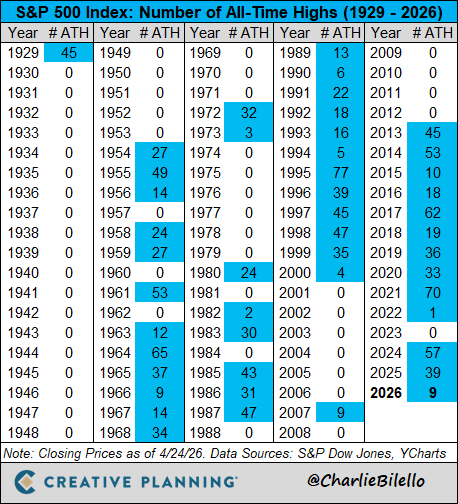

The S&P 500 closed at an all-time high on Friday, rising for a 4th consecutive week, its longest weekly winning streak since 2024.

The semiconductor index extended its winning streak to a record 18 consecutive positive sessions, and is now the most overbought in history.

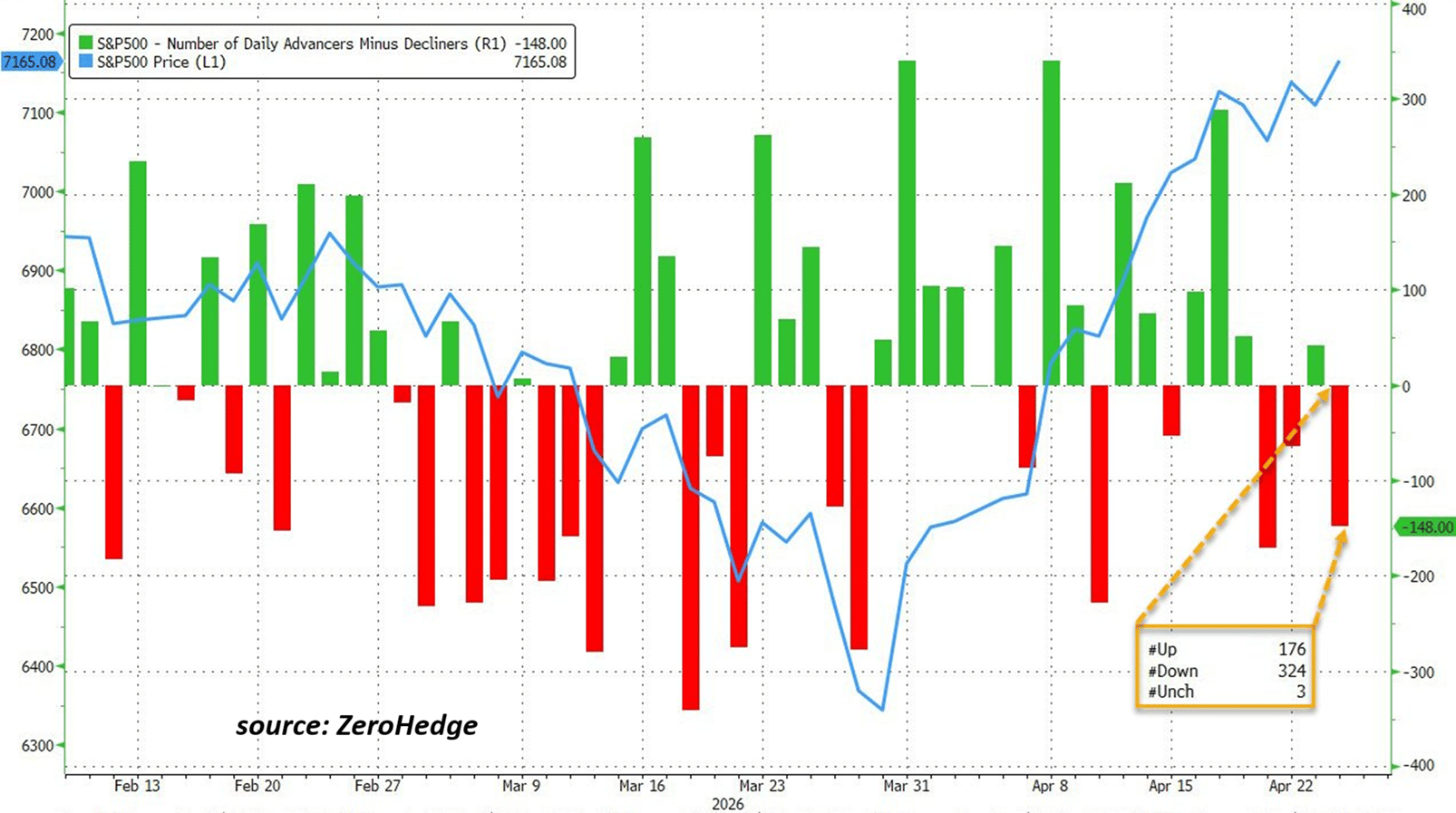

Despite the index closing at record highs, market breadth remains weak, with 62% of S&P 500 stocks, or ~320 names, closing in the red on Friday.

This marks the 2nd-worst breadth reading on a record-high close, surpassed only by October 28, 2025, when 80% of S&P 500 stocks closed in the red on the same day the index set a record.

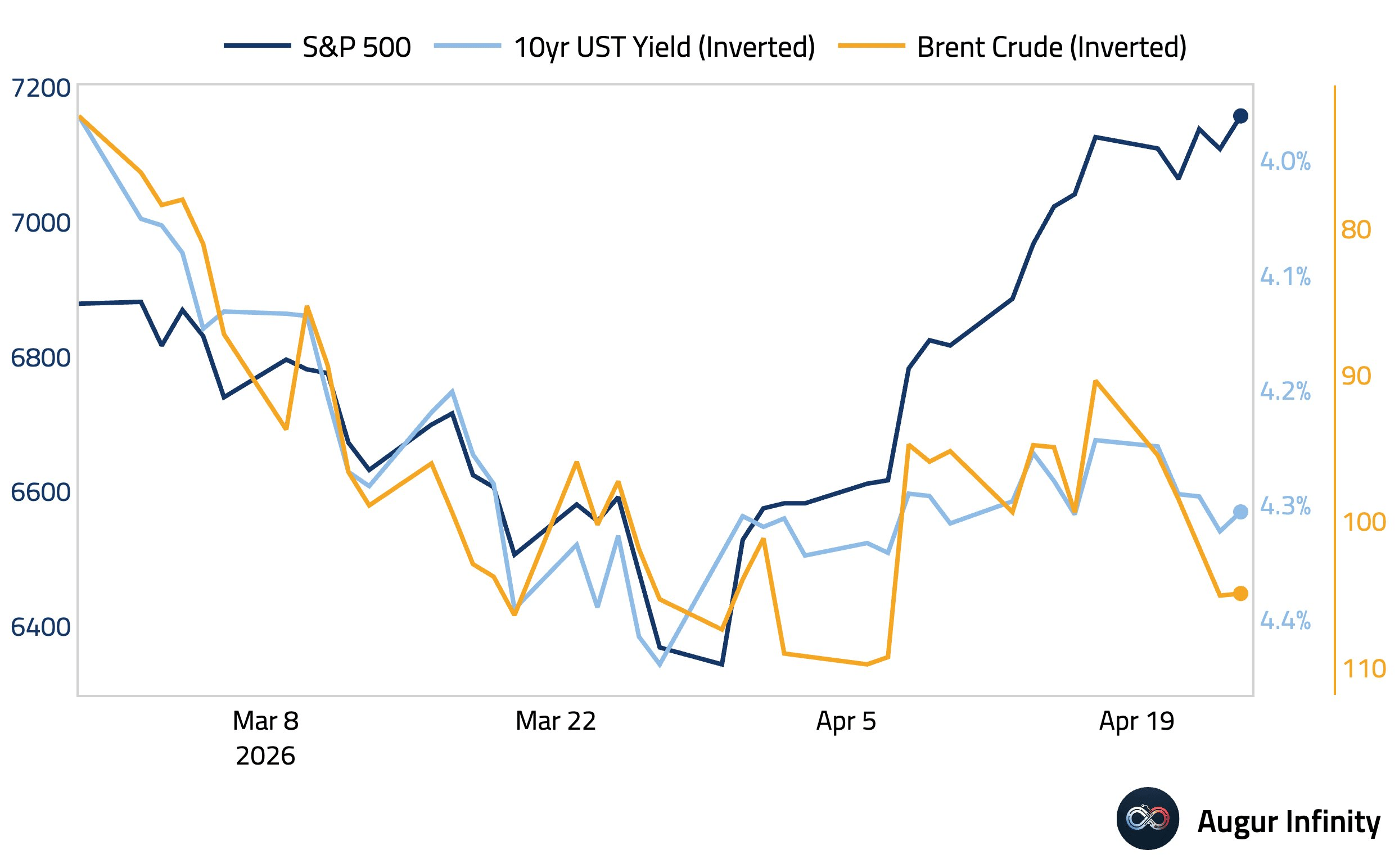

US crude and Brent oil rose to ~$94 and $105 per barrel last week, while Treasury yields declined after the Justice Department closed its probe into Federal Reserve Chair Jerome Powell, raising the prospect of rate cuts under a potential new Fed leadership.

Meanwhile, gold and silver had their worst week since mid-March.

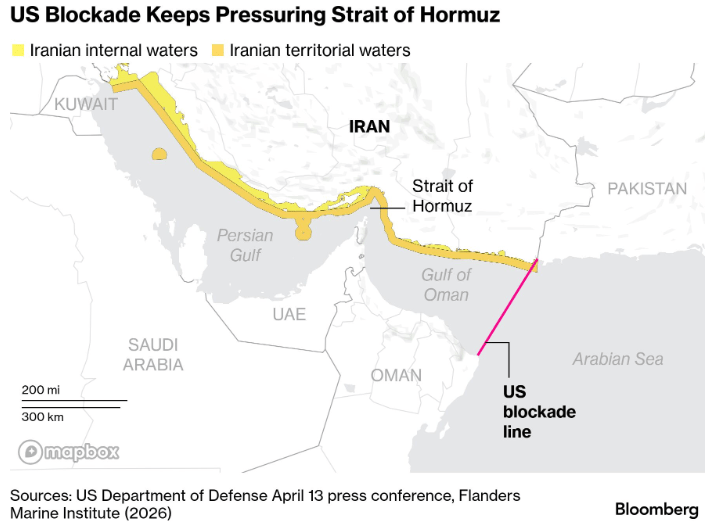

Overall, US-Iran peace talks have stalled as the conflict approaches its two-month mark.

Trump canceled the planned trip of his envoys Jared Kushner and Steve Witkoff to Pakistan on Saturday, saying Iran had "offered a lot, but not enough" and that too much time was being wasted on travel.

Iran's President Pezeshkian responded by stating his country will not negotiate under threats or while the US naval blockade remains in place, with Iranian Foreign Minister Araghchi departing Islamabad well before the US delegation was set to arrive.

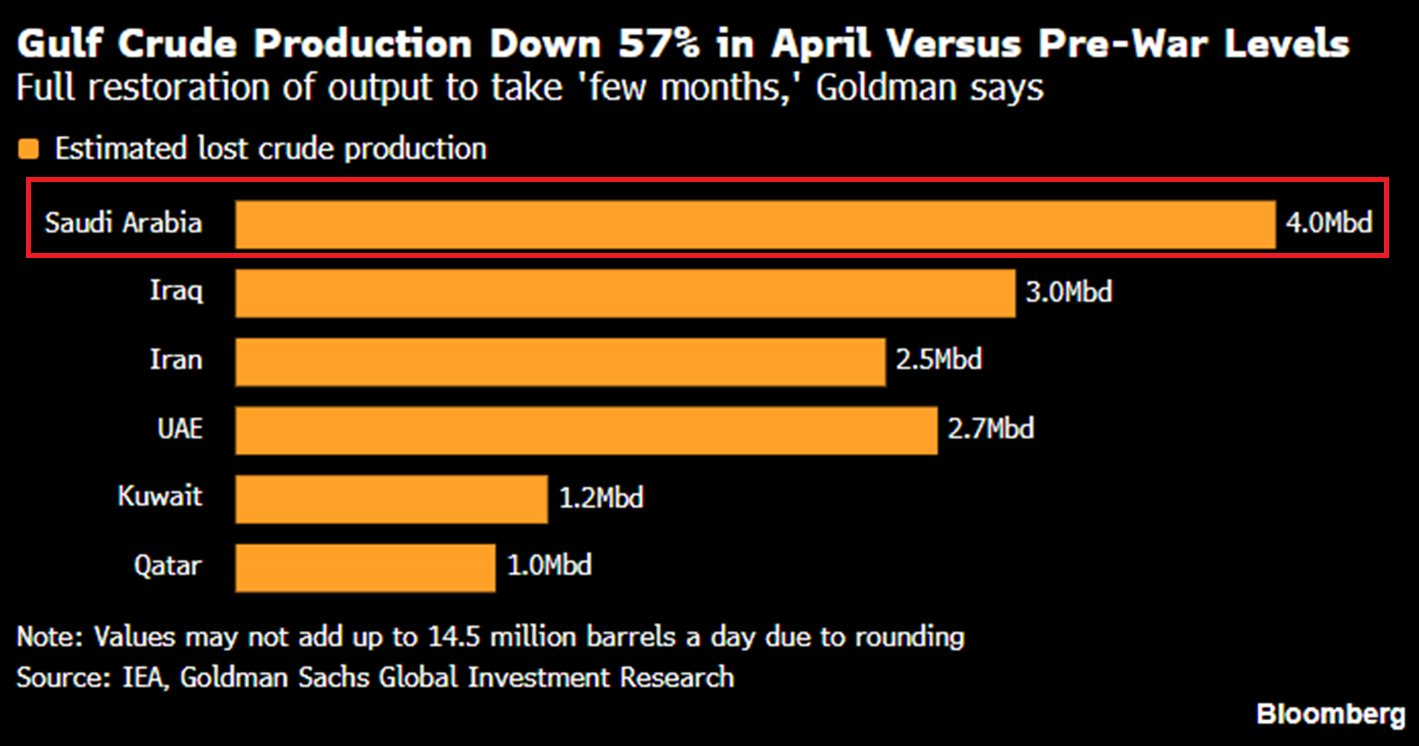

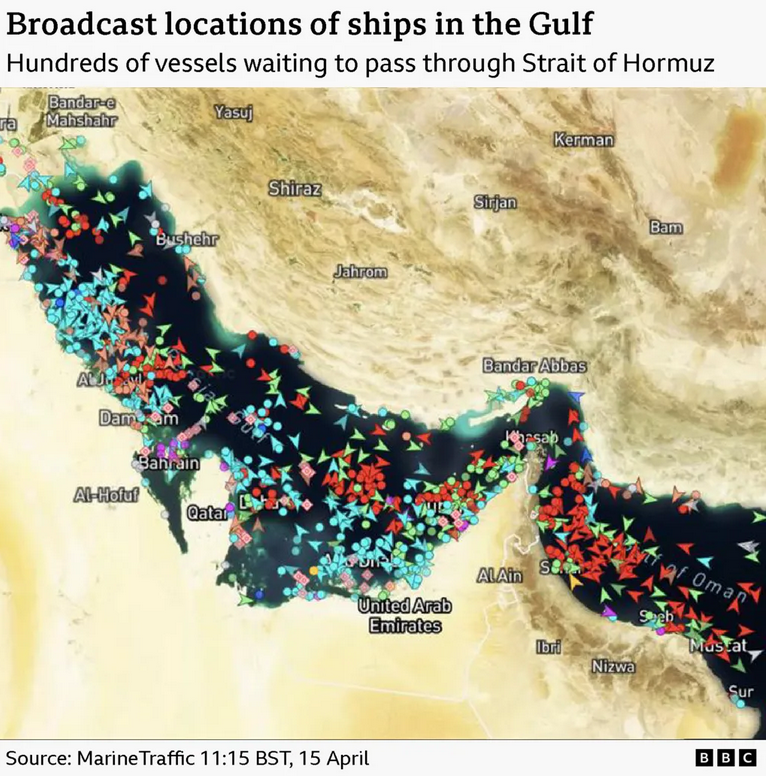

While the ceasefire has largely held since early April, both sides are maintaining rival blockades of the Strait of Hormuz, keeping ~a 5th of global oil flows effectively frozen in what the IEA has called the largest oil supply shock in history.

Araghchi is now traveling to Oman and Russia, with part of his delegation returning to Tehran to seek guidance on ending the war before rejoining him in Islamabad.

The path to a deal remains narrow, with Iran demanding the blockade be lifted before any talks and the US showing no sign of easing pressure.

Every day without a deal is another day of lost oil supply the world cannot afford.

In case you missed it, other posts from this week are listed below.

1) Weekly performance. In the first post attached, you can see last week’s performance of the major US indexes, the VIX volatility index, 10-year Treasury yield, the US Dollar, gold, silver, WTI Crude oil, and Bitcoin.

- S&P 500 +0.6%

- Nasdaq +1.5%

- Russell 2000 (small caps) +0.3%

- Dow Jones -0.4%

- US 10-year Treasury yield +6 basis points

- Bank Index -1.2%

- VIX +7%, front-month contract VIX futures +3%

- US Dollar index +0.5%

- Gold -3.2%

- Silver -7.5%

- WTI Crude Oil +13%

- Bitcoin +0.4%

1,000+ Proven ChatGPT Prompts That Help You Work 10X Faster

ChatGPT is insanely powerful.

But most people waste 90% of its potential by using it like Google.

These 1,000+ proven ChatGPT prompts fix that and help you work 10X faster.

Sign up for Superhuman AI and get:

1,000+ ready-to-use prompts to solve problems in minutes instead of hours—tested & used by 1M+ professionals

Superhuman AI newsletter (3 min daily) so you keep learning new AI tools & tutorials to stay ahead in your career—the prompts are just the beginning

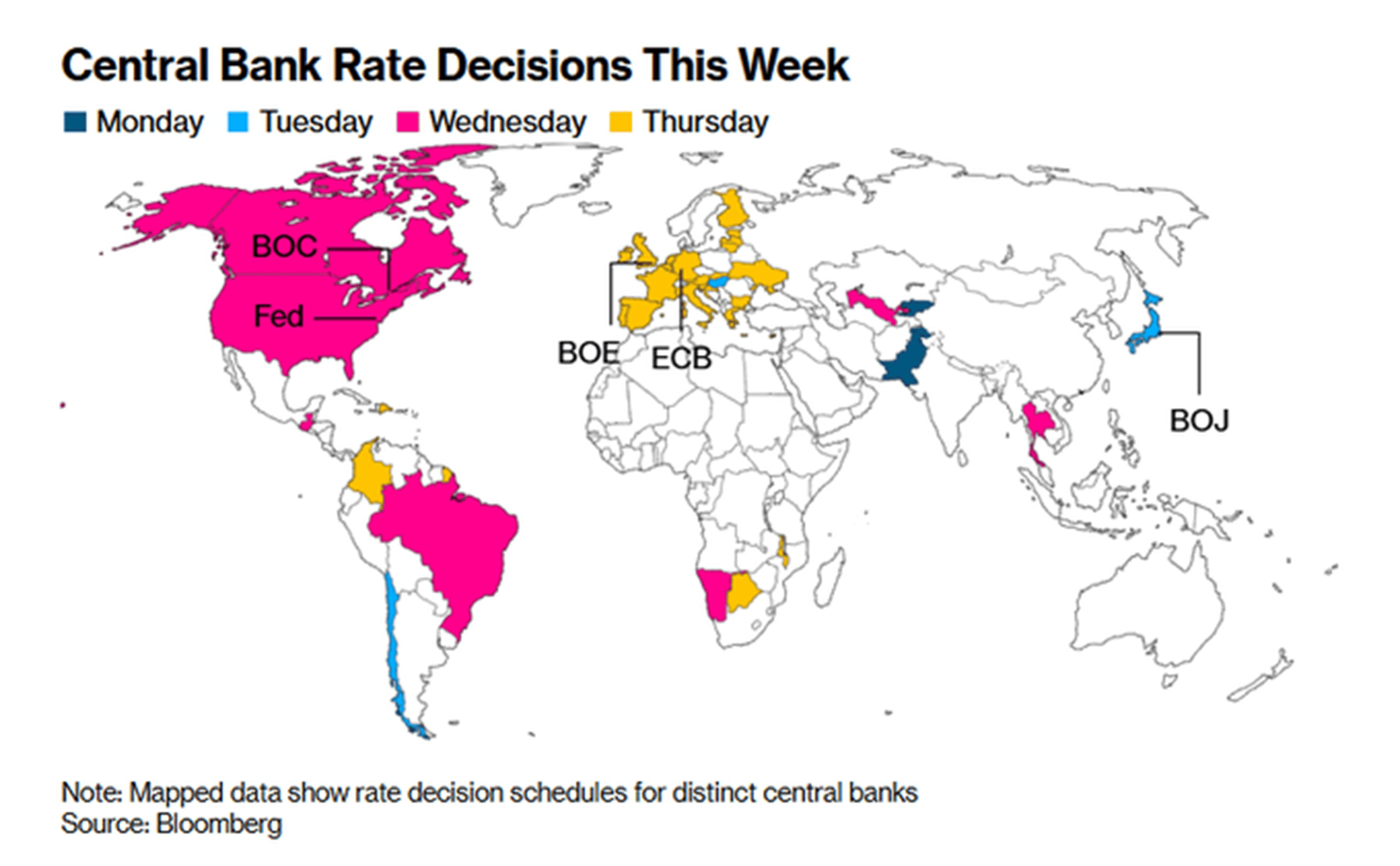

For the trading week ending May 1, key events are:

- US Housing Starts for March on Wednesday

- Fed interest rate decision on Wednesday

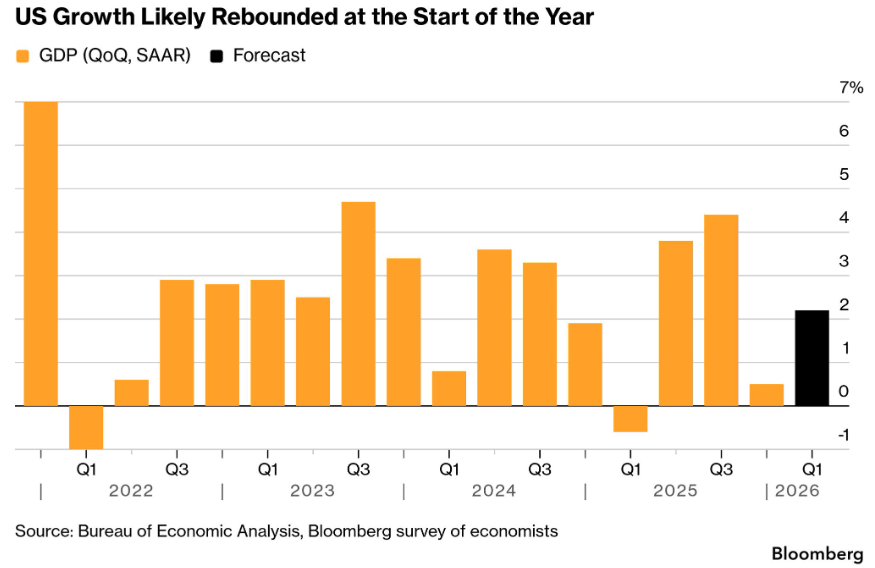

- US Q1 2026 GDP data first estimate on Thursday

- US ISM Manufacturing PMI for April on Friday

- ~40% of S&P 500 companies report quarterly earnings, including 5 of the Magnificent 7.

Microsoft $MSFT ( ▲ 2.13% ) , Alphabet $GOOGL ( ▲ 1.63% ) , Amazon $AMZN ( ▲ 3.49% ) , and Meta, $META ( ▲ 2.41% ) , report on Wednesday, followed by Apple, $AAPL ( ▼ 0.87% ) , on Thursday.

Investors will be focused on CAPEX plans for AI infrastructure, with the Magnificent 7 under pressure to justify their performance.

The Federal Reserve also meets on Wednesday in what could be Jerome Powell's final meeting as chair, with his term set to end on May 15 and Kevin Warsh awaiting Senate confirmation as his successor.

The Fed is widely expected to hold rates steady, with markets now pricing in less than 1 rate cut by December, down from at least 2 cuts expected before the Iran war began.

Moreover, the Bank of Canada meets alongside the Fed on Wednesday, while the European Central Bank, Bank of England, and Bank of Japan all announce rate decisions on Thursday.

Q1 2026 GDP and the Fed's preferred inflation gauge, the PCE Price Index, are also scheduled next week, offering the first concrete look at the Iran war's economic impact.

Next week is going to be huge.

2) What is happening with US semiconductor stocks? Is the pullback imminent?

3) Hedge funds are dumping US tech stocks at a furious pace.

4) Global government debt has never been higher.

5) Some additional posts covering interesting economic and financial market data: the US private credit selloff, nuclear power capacity by country, wheat prices, Asia oil imports, Corporate America cutting jobs at an accelerating pace, Wall Street and Main Street never being this far apart, and America's deepening demographic crisis.

Reply