- Global Markets Investor

- Posts

- ⚠️CHART OF THE WEEK: The real energy market shock is in fuel prices, not crude oil

⚠️CHART OF THE WEEK: The real energy market shock is in fuel prices, not crude oil

The real economic damage is already spreading through nearly all world economies

Global Markets Investor

March 21, 2026

In partnership with

GLOBAL MARKETS INVESTOR’S PORTFOLIO IS 🔥UP +97%🔥SINCE JANUARY 2024

DURING THE MARCH-APRIL 2025 MARKET TURMOIL, MAJOR US INDEXES FELL NEARLY 20%, WHILE THE GMI PORTFOLIO GAINED OVER 5%, FIND OUT HOW BELOW:

While WTI crude is up ~70% since January, the cost of refined petroleum products that consumers and businesses actually pay for has surged far more

Diesel wholesale prices are up +109% year-to-date, the largest increase among all fuel types.

Fuel oil wholesale is up +102%, while jet fuel and gasoline are both up +84%.

Speed Doesn’t Replace Strategy.

AI can surface the numbers in seconds, but numbers alone don’t create clarity.

In fact, many leaders have more financial data than ever yet less clarity about what to do next.

The real challenge isn’t reporting. It’s interpretation. Context. Judgment.

BELAY created the free guide The Future of Financial Leadership to explore why automation is a tool — not a replacement — for experienced financial oversight.

Inside, you’ll learn how the right human support brings structure to your numbers, confidence to your decisions, and focus to your growth strategy.

At BELAY, our U.S.-based Financial Experts help leaders move beyond dashboards and into decisive action.

Because insight doesn’t drive a business forward. Leadership does.

These are the prices that directly hit the economy, from what Americans pay at the pump, to airline ticket costs, to shipping and freight rates across the country.

By comparison, WTI Crude oil at ~$98 per barrel is the most widely quoted benchmark, but it only reflects the cost of unrefined crude in Texas, not the actual cost of the fuels that power the economy.

As fuel prices continue to surge at this pace, the inflationary impact on the US economy will be far greater than what crude oil benchmarks alone suggest.

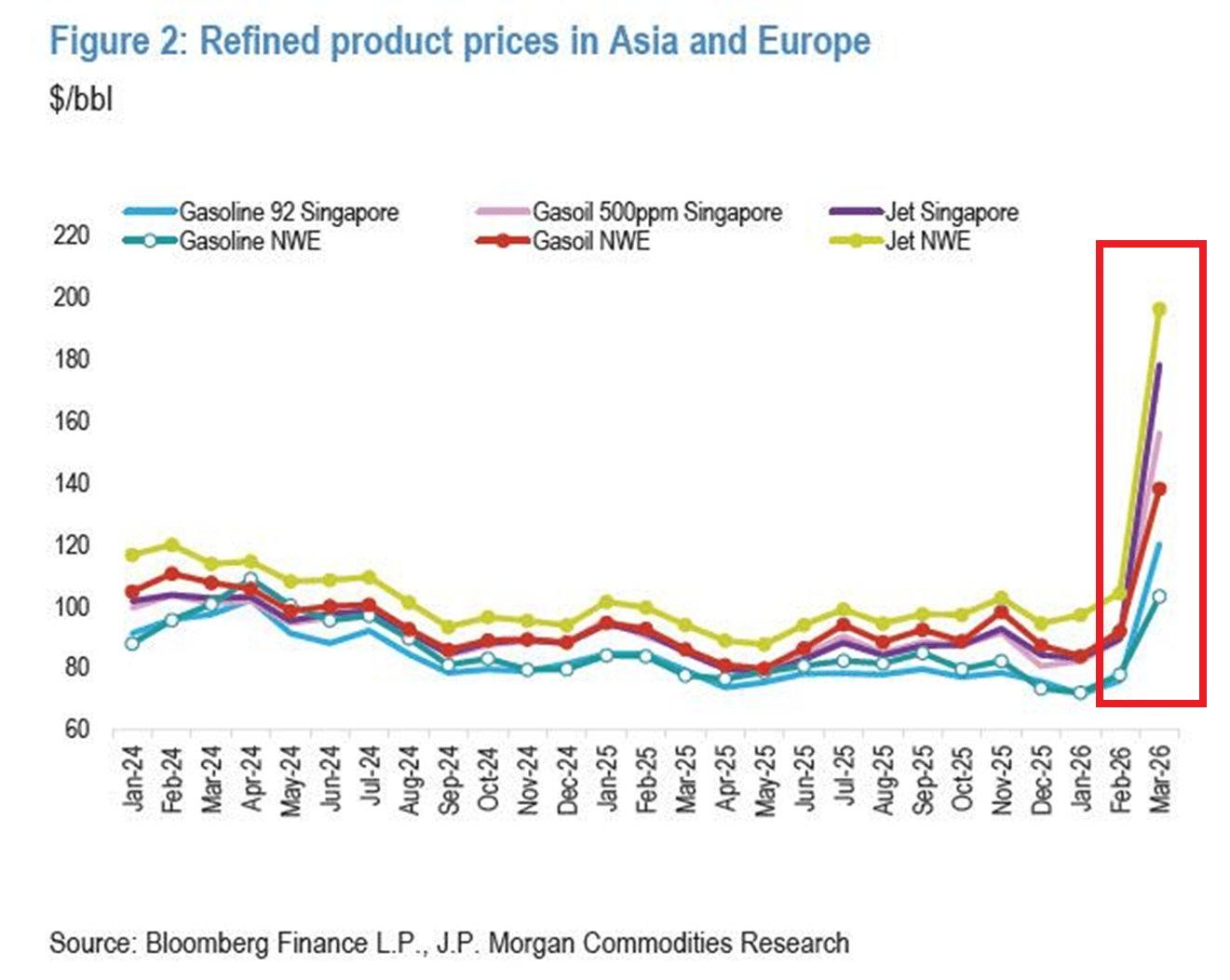

Gasoline and Jet fuel prices in Asia and Europe are also skyrocketing.

Jet fuel prices have more than doubled since the Iran War Started, reaching ~$200 per barrel in both Singapore and Northwest Europe.

Gasoline and diesel prices have also spiked, with gasoil in Singapore and Europe jumping to ~$150 per barrel, nearly doubling.

As a result, Airlines are canceling routes and adding $125-$200 surcharges per passenger as jet fuel costs make many flights uneconomic, with SAS and Air New Zealand already cutting services.

Furthermore, Governments across Asia are responding with emergency measures, including 4-day workweeks in the Philippines and Sri Lanka, school closures in Pakistan, and alternating driving days in Myanmar.

Here is also the convenient list of European countries acting on surging energy prices.

Meanwhile, Oil refiners are paying record premiums to replace increasingly missing Middle Eastern crude.

At one point the Brent oil futures spread, the gap between the 1-month and 6-month contract, surged to $20.95 per barrel on March 20, signaling extreme near-term supply tightness.

In simple terms, buyers were willing to pay ~$21 more per barrel for immediate delivery vs. delivery 6 months from now, a level almost never seen in the oil market.

Furthermore, physical crude premiums exploded across the globe, with Southeast Asian grades like Malaysia's Labuan and Indonesia's Minas trading at +$10 above Brent, up from ~$1-2 under normal conditions.

All while US crude oil delivered into Asia is now carrying premiums of +$12 to +$15 per barrel, while Norway's Johan Sverdrup hit a record +$11.30 above Brent on Thursday.

The problem is that many Asian refineries were designed to process heavy crude oil from the Middle East and cannot easily switch to lighter alternatives from the US and Europe.

As a result, the few compatible replacement grades are seeing the biggest price spikes making total energy costs even worse.

Lastly, an important development, global floating oil storage is draining at an alarming rate.

Crude oil and condensate sitting on tankers along the Persian Gulf, Gulf of Oman, and key Asian shipping routes have nearly halved to just 78 million barrels, down from ~150 million barrels in late November.

As a reminder, Iranian barrels make up ~33% of remaining global floating storage, much of it anchored near the Gulf and on tankers en route to Asian refiners.

The stockpile has been declining by ~1.8 million barrels per day since the Iran War began, the fastest pace since 2020.

Estimates show there are ~131 million barrels of Russian and 105 million barrels of Iranian crude on the water, but combined, that would only offset ~2 weeks of disrupted Strait of Hormuz flows.

With the Strait effectively closed for 3 weeks and floating storage nearly halved, the global oil buffer is running out fast.

If this pace continues, the market will have almost no cushion left against further supply shocks, and oil prices could surge well beyond current levels.

To sum up, this is no longer just an oil disruption, it is an industrial shock spreading across the entire world.

If you find it informative and helpful, consider a paid subscription or become a Founding Member, and follow me on Twitter or Nostr:

Reply